Additional information

Additional information

Sustainability Statement Appendix

General

Structure of the materiality assessment

We conducted the DMA in three steps.

Step 1: Identifying potential material ESG topics

An important first step in the DMA was to gain insight into Gasunie’s value chain and the company’s position within it. Based on this analysis, we identified relevant impacts, risks and opportunities in the subsequent steps of the DMA.

We compiled a longlist of potential material topics. In addition to Gasunie’s business context, we also took into account the corporate and sustainability strategy, the results of the 2024 DMA, material topics reported by peers in their annual reports and input from internal stakeholders.

Step 2: From longlist to medium list – screening for relevance and IROs

The second step saw us screen the longlist down to a medium list by assessing the potential material topics for relevance to Gasunie and its stakeholders. Topics that did not involve a potential impact, risk or opportunity (IRO) were excluded. To identify potential material IROs, we interviewed internal experts, i.e. colleagues with specific expertise, such as an ecologist, local community manager, procurement consultant, HR consultant and a corporate legal affairs and corporate governance expert. Their insights were a valuable basis for further narrowing down the medium list.

Step 3: from medium list to shortlist of material topics and identifying inside-out and outside-in impact

The third step consisted of whittling the medium list down to a shortlist. The items on the medium list were validated with internal and external stakeholders, which saw us interview the Natuur & Milieu environmental organisation, the Dutch Ministry of Finance and members of the Executive Board and Supervisory Board. This produced a shortlist.

We held workshops to gather input on the inside-out and outside-in impact of the shortlisted topics and IROs. We selected participants for these workshops based on their areas of expertise to ensure they could provide relevant input. Based on the input that emerged from the workshops, we assessed both the impact materiality and financial materiality of the IROs. As part of our DMA, we also looked at how impacts, dependencies, risks and opportunities for the organisation relate to each other. These interrelations were taken into account in determining which sustainability topics are material for our reporting.

Impact materiality and financial materiality were determined based on the following factors:

Impact materiality:

- Scale: How bad is the impact?

- Scope: How big is the impact?

- Remediability: To what extent are we able to mitigate or repair the adverse impacts by taking corrective measures?

- Likelihood: how likely is it that the impact will occur?

Financial materiality:

- Financial impact: What are the financial consequences attached to the opportunity or risk? These can be direct costs or monetary benefits, but also indirect costs, such as reputational damage or potential revenue losses or increases.

- Likelihood: How likely is it that the risk will materialise?

By setting a threshold, we were able to separate material from non-material IROs. We consider an IRO to be ‘material’ if it scores high from an impact perspective and/or a financial perspective. To obtain external validation of the DMA results, we asked our key external stakeholders to provide feedback. The material topics were subsequently submitted internally for validation to the CSRD steering committee consisting of six department managers. Finally, the DMA results were approved by the Executive Board.

Energy transition

Our contribution to the National Transition Pathway

We have calculated the extent of Gasunie’s influence over the coming years on the Dutch ‘transition pathway’, i.e. on the way to full decarbonisation. This is our fifth time calculating this.

Under Our contribution to the National Transition Pathway in the ‘Energy transition’ section of this report, we show the impact of the investments we intend to make between now and 2030, and through to 2035 on greenhouse gas emissions in the Netherlands. We show what our influence on the transition pathway is and the average carbon emissions reduction rate the Netherlands must maintain to become net-zero by 2050.

The more Gasunie’s sustainability projects are completed on time, the greater the volume of green energy and captured CO2 we can start transporting for our customers. This increased sustainability will likely be accompanied by a decrease in the amount of fossil energy we transport. In the visuals presented in the section referred to above, we show the net emissions17 (the carbon footprint) of all the energy and the negative emissions from the CO2 we transport to and from parties in the Netherlands on behalf of third parties. Reducing these emissions is made possible in part by feed-in parties, customers and project partners of Gasunie.

17 With net-zero emissions there may still be natural gas consumption, for example, because CO2 emissions from fossil fuels are being captured through CCS.

We only take into account the gases transported through the Gasunie network; we have not taken into account the contribution made by biomethane in the networks of the regional network operators, for example. Nor do we include any negative emissions from biomethane production. For hydrogen we have only included green hydrogen and imports; to avoid any double counting with CCS projects we have disregarded blue hydrogen.

To determine the contribution that will be made through our investments in biomethane and hydrogen, we assume that these will replace natural gas. This assumption results in a somewhat conservative estimate given that, if biomethane and hydrogen were to replace oil and/or coal, for example, the emission reduction contribution would be greater still. For CCS projects, the expected transport volumes of captured CO2 from the Netherlands have been used; we have not included any storage of CO2 from neighbouring countries in our calculations. Upstream emissions in the value chain are not included.

The emission reduction is determined relative to the situation in the base year 2023. We use the Climate and Energy Outlook report of current and intended policy published by the Netherlands Environmental Assessment Agency PBL as a reference for all external developments (outside Gasunie’s sustainability projects). For the years up to 2030, we use the 2025 edition of the Climate and Energy Outlook (link). For the years beyond 2030, we used the 2024 edition of the Climate and Energy Outlook (link), as the latest edition does not provide data for the post-2030 period. We use a natural gas emission factor of 56.2 kg/GJ (link).

In the figures, we only take into account the emission savings in the Netherlands. Gasunie’s energy transition investments can also contribute to emission reduction abroad, for example, through the transport of foreign CO2 for storage in the Netherlands (cutting 1.5 Mt in emissions by 2030).

Because Gasunie is also active in Germany, we have also included the emission reduction effect of our proposed investments for the German hydrogen network (Hyperlink) in the table. However, we do not include this effect when calculating our impact on the national transition pathway for the Netherlands. We have not calculated or visualised Gasunie’s impact on Germany’s national transition pathway, because the impact we can make in Germany is much smaller than in the Netherlands, where we are the sole natural gas TSO.

In this report we only consider the impacts of our investments between 2020 and 2030 or 2035. A new series of Gasunie investments for the period after that could lead to a steeper decline along the Dutch transition pathway.

The following two visuals provide a detailed forecast of our expected contribution to carbon emission reduction across Dutch society, as currently projected (2025 annual report), compared to the previous year (2024 annual report).

We now expect our energy transition projects to enable users to cut 7.8 Mt of carbon emissions by 2030, compared to our estimate of 16.4 Mt in last year’s annual report.

The following two visuals provide a detailed forecast of our expected contribution to carbon emission reduction across German society, as currently projected (2025 annual report), compared to the previous year (2024 annual report).

We now expect Hyperlink, i.e. our share in Kernnetz, to be able to facilitate a reduction of 1.3 Mt by 2030 (forecast from last year’s annual report: 4.4 Mt by 2030).

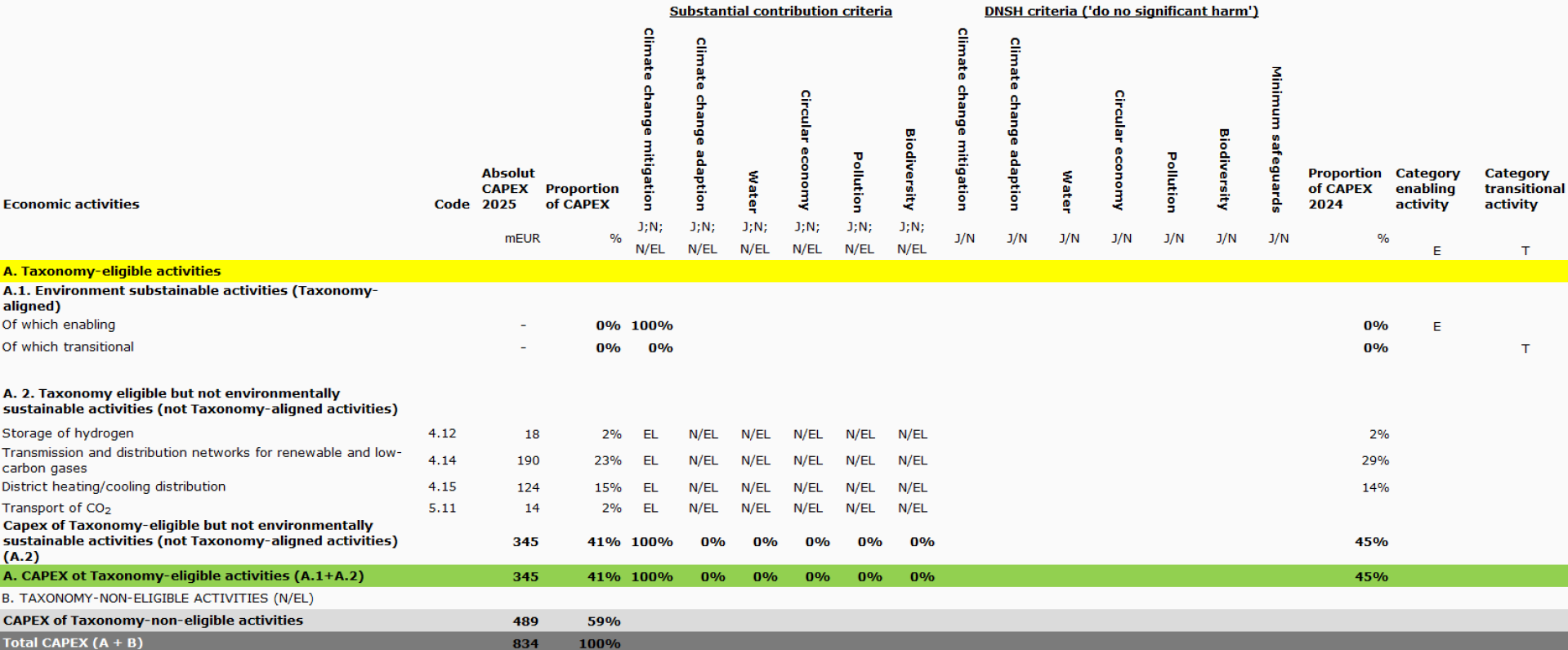

Taxonomy

The EU Taxonomy tables are based on the consolidated financial statements. All of our eligible activities are allocated to activities associated with the climate change mitigation objective, meaning that there is no question of claiming multiple climate objectives for one and the same activity. We have chosen not to apply the Delegated Regulation amending the Delegated Taxonomy Regulations of 4 July 2025 earlier than proposed in the European Commission’s Questions and Answers on EU Taxonomy simplifications.

Capex KPI

We calculated the share of Taxonomy-eligible economic activities in our investments in capital goods (CAPEX) by dividing the CAPEX of these activities (numerator) by the total CAPEX (denominator). The numerator and denominator include our investments in property, plant and equipment and intangible assets. In addition, we have described our investments in joint ventures through which Taxonomy-eligible activities are realised. The items mentioned above are further explained in note 4 ‘Property, plant and equipment’, note 5 ‘Intangible assets’ and note 7 ‘Investments in joint ventures’ to the consolidated financial statements.

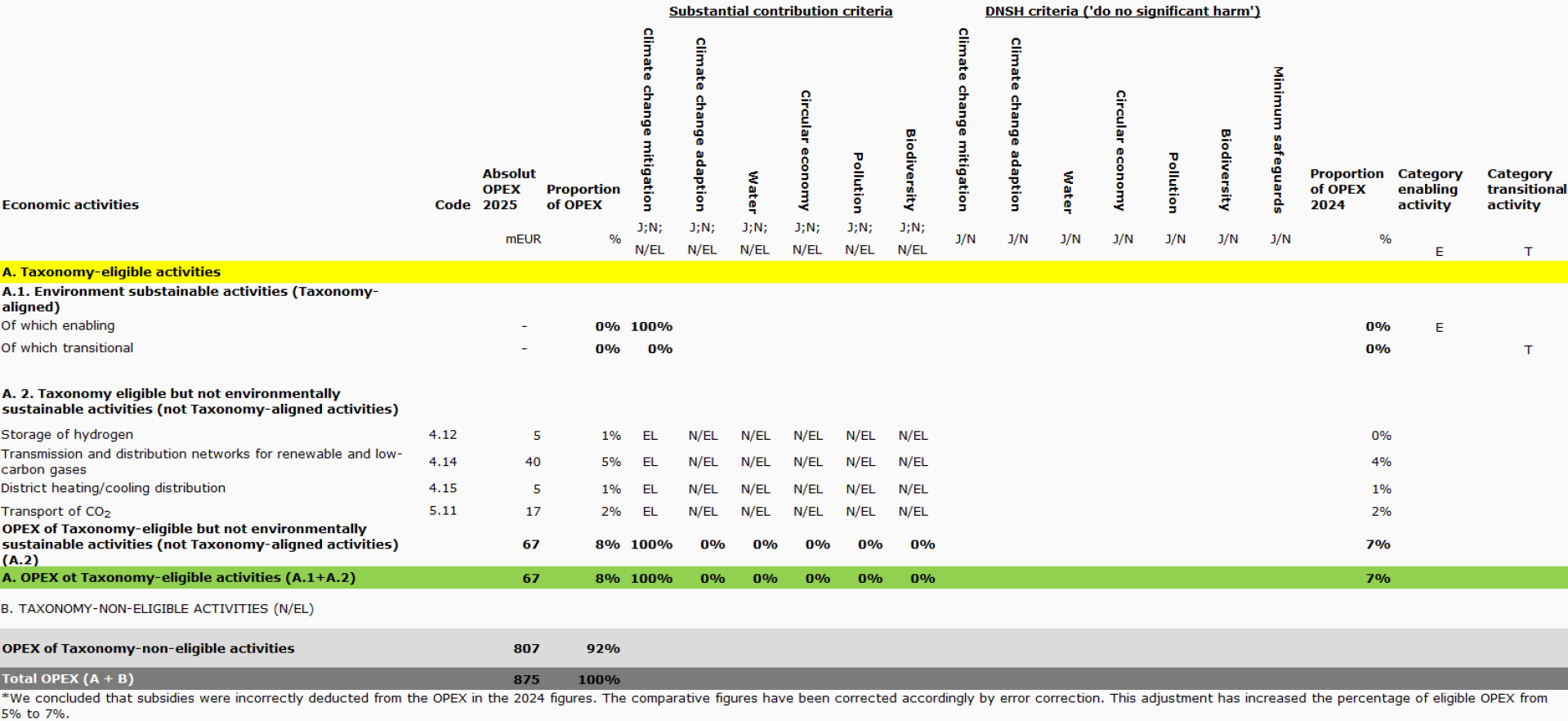

Opex KPI

We calculated the share of Taxonomy-eligible economic activities in our OPEX by dividing the OPEX of these activities (numerator) by the total OPEX (denominator). We included the personnel expenses and other expenses in the denominator, corrected for costs attributed to investments and overhead costs.

The other costs also include the cost of network operations, which mainly concerned the procurement of nitrogen production capacity and electricity for the production of nitrogen and the cost of electricity and gas for gas transport and storage operations. These costs are inextricably linked to the uninterrupted and effective operation of our assets.

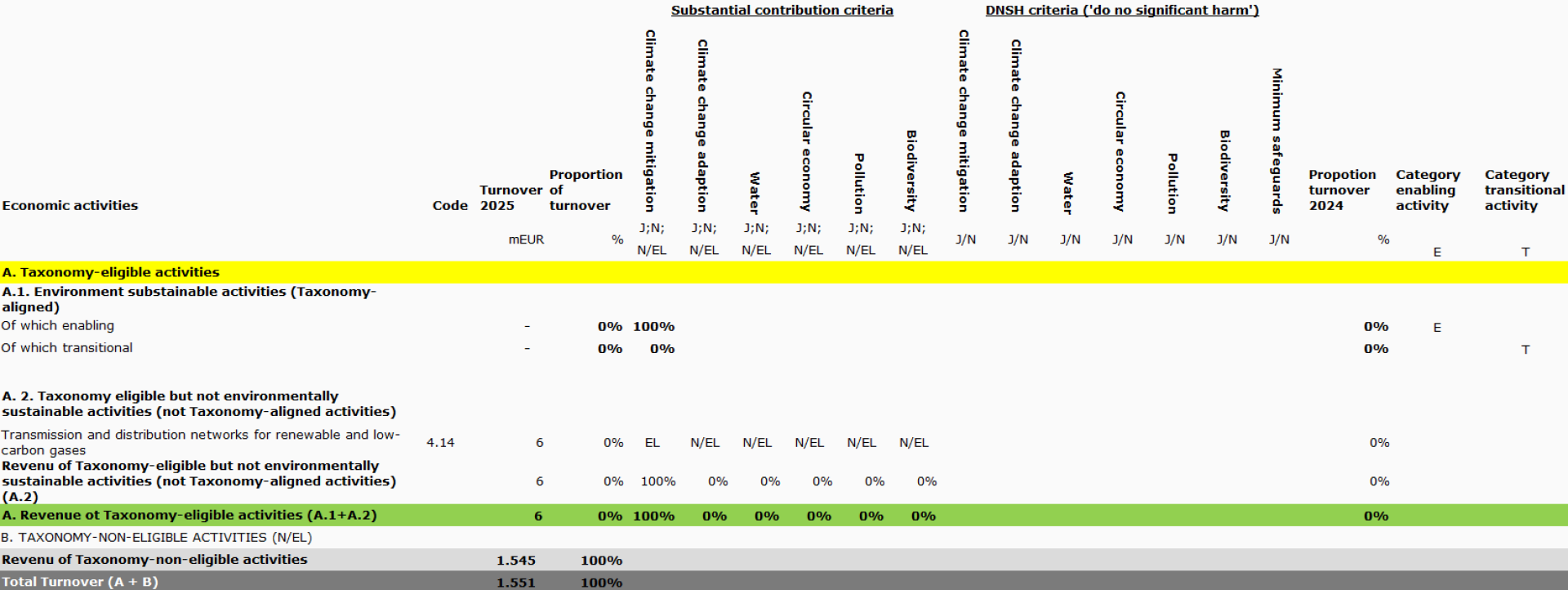

Revenue KPI

We calculated the share of Taxonomy-eligible economic activities in our total revenue by dividing the revenue from Taxonomy-eligible activities (numerator) by the total net revenue (denominator) as specified in the consolidated statement of profit or loss for 2025. The accounting policies used with regard to net revenue are explained in more detail in the consolidated financial statements.

Activities related to nuclear energy and fossil gas

| Nuclear energy | ||

| 1 | The undertaking carries out, funds or has exposures to research, development, demonstration and deployment of innovative electricity generation facilities that produce energy from nuclear processes with minimal waste from the fuel cycle. | No |

| 2 | The undertaking carries out, funds or has exposures to construction and safe operation of new nuclear installations to produce electricity or process heat, including for the purposes of district heating or industrial processes such as hydrogen production, as well as their safety upgrades, using best available technologies. |

No |

| 3 | The undertaking carries out, funds or has exposures to safe operation of existing nuclear installations that produce electricity or process heat, including for the purposes of district heating or industrial processes such as hydrogen production from nuclear energy, as well as their safety upgrades. |

No |

| Fossil gas | ||

| 4 | The undertaking carries out, funds or has exposures to construction or operation of electricity generation facilities that produce electricity using fossil gaseous fuels. | No |

| 5 | The undertaking carries out, funds or has exposures to construction, refurbishment, and operation of combined heat/cool and power generation facilities using fossil gaseous fuels. | No |

| 6 | The undertaking carries out, funds or has exposures to construction, refurbishment and operation of heat generation facilities that produce heat/cool using fossil gaseous fuels. | No |

Emissions

For the consolidation of our GHG emissions (Scopes 1, 2 and 3) we use the operational control approach, which means that, in addition to including our group companies and joint operation (BBL Company) in the consolidation, we also include the GHG emissions of our EemsEnergyTerminal joint venture. We have included the emissions of joint ventures over which we have no operational control in Scope 3 (category 15).

To be able to add up the impact of the various GHG emissions, emissions relating to each particular gas are converted to CO2e (carbon dioxide equivalent). The emission factors we use for this are taken from reputable databases, such as emissiefactoren.nl for the Netherlands and international equivalents, where applicable, such as DEFRA (the UK’s Department for Environment, Food & Rural Affairs) and DEHst (German Emissions Trading Authority). Our greenhouse gas emissions are not just strictly methane emissions: they include CO2 emissions caused by combustion of fossil fuels and, to a minor degree, also refrigerants, SF6 and diesel.

Scope 1 and 2 emissions

We use Guarantees of Origin (GOs) to prove the renewable source of the electricity. In the Netherlands, Gasunie purchased GOs from European wind farms in 2025. In Germany, Gasunie procured green electricity directly from its electricity supplier. In total, we compensated 99.1% of our total Scope 2 emissions (2024: 99.7%).

In 2025, we decarbonised 9,000 MWh of our natural gas consumption using Guarantees of Origin (GOs) (2024: 40,873 MWh). We have not deducted this amount from our Scope 1 emissions disclosed in the Scope 1, 2 and 3 ESRS tables18.

18 Biomethane is not covered by the system of Guarantees of Origin because there is no internationally recognised certification for biomethane. For now, the Greenhouse Gas Protocol does not yet allow the use of biomethane certificates for the reduction of Scope 1 and 3 emissions.

Scope 3 emissions

The following will provide a more detailed explanation of the Scope 3 categories that are significant to Gasunie. Categories 8, 9, 10, 11 and 14 are not part of our Scope 3 emissions because they do not apply to Gasunie’s business operations.

Category 2: Capital goods

This category includes all upstream (cradle-to-gate) emissions from the extraction, production and transport of capital goods (pipelines, equipment, IT hardware, buildings, facilities and vehicles) procured by Gasunie. Emissions for capital goods relate to all capital expenditures and therefore cannot be related to operating expenses that occur on an annual basis. Emissions associated with capital goods are attributed to the year when the expenditures occurred to guarantee consistency with financial reporting.

Category 1: Purchased goods and services

For Gasunie, this category is the second most prominent one of the Scope 3 categories. In this category, we record the emissions generated from the procurement of our goods (other than capital goods) and services. Emissions related to the procurement of nitrogen are also included in this category. Where possible, we make arrangements with suppliers for them to decarbonise their energy usage, including through the purchase of GOs, which pushes down emissions for the value chain as a whole. Other goods and services (pipeline materials, engineering and maintenance services, odorant, inspections using helicopters) are also significant contributors to emissions across the value chain. For the most dominant of these goods and services, i.e. pipelines, valves, IT, engineering services and contracting, we are in talks or will commence talks with suppliers on emission reduction.

Category 3: Fuel- and energy-related activities

This category includes emissions related to the extraction, production and transport of fuels and electricity purchased and consumed in the reporting year, which are not included in Scope 1 or Scope 2. All upstream emissions and transport and distribution losses of purchased fuel and electricity (wheel-to-tank) are reported in this category. This category also covers emissions caused by losses during the transmission and distribution of electricity and upstream emissions from methane leaks (as part of Scope 1).

Scope 3 emission calculation

For our Scope 3 emission calculations for 2025, we were able to obtain primary data that covers 48% of our Scope 3 emissions (2024: 35%, 2023 (base year): 41%). Wherever primary data was not available or not available in time, we used secondary data. The increase in the percentage of primary data is the result of the fact that in 2025 we procured more (capital) goods and services (categories 1 and 2) for which primary data was available. Implementation of our supplier engagement programme has also led to us receiving more primary data for our Scope 3 reporting this year. The aim in the long term is to keep improving data quality and reducing data uncertainty, so that we can ultimately track our performance as effectively as possible.

The methodology we applied in 2025 has not changed compared to 2024 and 2023 (base year). Given that the recent update to the DEFRA database has a material impact on our Scope 3 emissions, we have recalculated the comparative figures for the 2024 and 2023 (base year) emission years. We applied three different methods to map our Scope 3 emissions:

- Spend method: Emissions are determined based on the spend of the relevant categories. Procurement data (in euros) is combined with emission factors from the most recent DEFRA database (2022), corrected for inflation based on data from Statistics Netherlands.

- Volume basis: Emissions are determined based on the actual ‘volume’ of the product or service (for example: kilograms, distance travelled, amount of energy used). Data from our suppliers is combined with emission factors from CO2-emissiefactoren.nl (2025).

- Supplier specific: Emissions are calculated by our suppliers. Emissions from publicly available annual reports or sustainability statements are multiplied by the ratio of our spend to a supplier’s total revenue. In 2025, we received emission data for several of our suppliers directly from those suppliers. Our aim is to get more data directly from suppliers over the coming years.

| Calculation method | ||||

|---|---|---|---|---|

| Scope 3 category | Description of emission source | Supplier specific | Volume basis | Spend method |

| Category 1: Capital goods Categorie 2: Purchased goods and services |

Emissions from the production of purchased steel materials (related to the production of steel pipes, valves, flanges, and so on) | x | x | |

| Emissions from purchased construction services (occurring on our construction sites) | x | x | ||

| Emissions from production of purchased nitrogen | x | |||

| Other purchased products/services | x | |||

| Category 3: Fuel and energy-related activities | All emissions from production and transportation of purchased fuel and energy | x |

Energy consumption and mix

Our energy consumption and mix

| Energy consumption and mix in MWh | 2025 | 2024 |

|---|---|---|

| Consumption of energy from fossil sources | ||

| Consumption of fuel from coal and coal products | - | - |

| Consumption of fuel from crude oil and petroleum products | 7,522 | 8,975 |

| Consumption of fuel from natural gas | 1,237,035 | 1,295,517 |

| Consumption of fuel from other fossil sources | - | - |

| Consumption of purchased or obtained electricity, heat, steam, and cooling from renewable sources | 29,192 | 25,701 |

| Total consumption of energy from fossil sources | 1,273,749 | 1,330,194 |

| Share of consumption of energy from fossil sources (%) | 60% | 61% |

| Consumption from nuclear sources | - | - |

| Share of consumption from nuclear sources in total energy consumption (%) |

0% | 0% |

| Consumption of energy from renewable sources | ||

| Consumption of fuel from renewable sources, including biomass | 67 | 65 |

| Consumption of purchased or obtained electricity, heat, steam, and cooling from renewable sources | 856,265 | 833,794 |

| Consumption of self-generated energy | 1,957 | 4,070 |

| Total consumption of energy from renewable sources | 858,289 | 837,930 |

| Share of consumption of energy from renewable sources (%) | 40% | 39% |

| Total energy consumption | 2,132,038 | 2,168,124 |

Biodiversity

Since Gasunie operates both onshore and offshore, its construction and expansion of infrastructure may disturb (marine) habitats, with possible consequences such as biodiversity loss. In addition, permitting procedures constitute a transition risk, as Gasunie is required to carefully assess and mitigate ecological impacts, including nitrogen deposition, for every new project. The double materiality assessment revealed several impacts, risks and opportunities in this domain:

| No. | ESRS | Material topic - ESRS | IRO |

|---|---|---|---|

| 4 | E4 | Biodiversity | Potential negative impact: For the purpose of the energy transition, Gasunie may build and operate more infrastructure on land and at sea in the future. Construction at sea/on land may lead to disruption of marine and other habitats, resulting in possible loss of biodiversity through habitat disruption, noise and pollution. |

| 5 | E4 | Biodiversity | Transition risk: Gasunie depends on obtaining permits from governments and other competent authorities for its current and future projects. These permits are necessary to start or continue infrastructure projects. When applying for permits, the impact on biodiversity must be included and - where necessary - mitigated. If these ecological impacts (including nitrogen deposition) are insufficiently investigated or addressed, the project may not meet the legal requirements or societal expectations. If biodiversity is not adequately considered in the permit process, this can lead to the revocation or refusal of permits with delays in project implementation (costs) and/or fines as a result. |

Policy

Our current biodiversity policy focuses on nature-inclusive design, construction, operation and decommissioning. Gasunie has drawn up guidelines to ensure that biodiversity-enhancing measures are implemented at the various project stages.

We embrace biodiversity as a material topic. At the same time, however, we recognise that further steps are needed to fully develop our biodiversity policy. In 2025, we began drafting a biodiversity action plan to align goals, policy and action plans. We will also seek to align this plan with our existing sustainability strategy.

Action plans

The actions needed to achieve our biodiversity goals will be detailed in the aforementioned biodiversity action plan.

Resources

In 2026, we will work out the resources we will need to implement the action plan.

Measurable targets

In 2026, we will determine which measurable targets we aim to achieve. In 2028, i.e. in our 2027 annual report, we want to publish our first comprehensive biodiversity disclosures in accordance with the ESRS E4 standard.

Circularity

Assumptions in calculating the kilograms of steel and recycled materials used for the steel procured

At the Procurement department, we record the amount of steel purchased (in kilograms) where possible, as well as the percentage of secondary reused or recycled materials contained within that steel. We calculate the weight of purchased pipelines based on available data. If weights for certain items are unknown and cannot be calculated, we extrapolate a figure based on expenditure.

The following assumptions were used in calculating the amount of steel purchased (in tonnes) and the proportion of secondary reused or recycled materials (in percentages and tonnes):

Assumptions in calculating kilograms of steel

- To determine the total weight in kilograms of procured steel, the following products were used: pipes, flanges, valves, pressure equipment and pressure vessels, bends and couplings.

- The assumption for calculating the weight of these products in kilograms is that they are made fully of steel.

- For pipes, the following method was used to calculate the weight in kilograms of a metre of pipe procured: Kg/meter = (R2 - (R -2 x WD) 2) x (π/4) x 1000 x 7850/1.000.000.000

R = outer radius; WD = wall thickness, π = pi (the mathematical constant, approx. 3.14159); 7850 = the density of steel; with 1000 and 1000000000 being conversion factors used to calculate the correct units. - The weights of flanges, valves, pressure equipment and pressure vessels, bends and couplings in kilograms was determined by linking the numbers of purchased items to the weights listed in the corresponding design drawings.

- If the weight of certain components cannot be determined or calculated due to missing information, an estimate is made by extrapolating from the calculated figures by product.

Assumptions for the kilograms of secondary reused or recycled materials used for procured steel

- Where available, Environmental Product Declarations (EPDs) are used to report the percentage of secondary materials.

- If no EPD is available, we use the percentage of secondary materials provided by the supplier (Mokveld).

- In the absence of supplier information, the EPD by Mannesmann Line Pipe is used. This pipe manufacturer also supplies to Gasunie through other suppliers. The percentage used (18%) is conservative compared to the typical amount of scrap added to the blast furnace process (15–25%).

Diversity

Actions

Inclusive and diverse leadership (MT)

Gasunie invests in HARRIE training courses

Gasunie has set itself the goal of creating permanent positions for talented people with poor prospects of finding a fulfilling job on the regular job market. Offering HARRIE training courses through CNV Jongeren is one way of providing the right guidance to achieve this. HARRIE is offered to anyone who would like to make themselves available as a buddy for a colleague with otherwise poor prospects of finding a fulfilling job, who perhaps needs different or just a little more guidance in their daily work compared to other employees. So this facility is explicitly not just for Gasunie managers. HARRIE is a Dutch initialism that stands for ‘Helpful, Alert, Calm, Realistic, Instructing and Honest’. By having multiple ‘HARRIES’, we ensure an inclusive and diverse organisation where the principle of equity is given a high priority.

Room for talent (MT)

Referral bonuses

Gasunie uses its own employees to attract talent through our referral programme. Our colleagues can give family, friends and acquaintances first-hand information about the jobs available at Gasunie and how they can also contribute to the energy transition. The referral programme is particularly useful as a tool for finding the right people for hard-to-fill positions. Our employees receive a bonus for bringing in new talent and can choose to either keep the bonus for themselves or donate it to charity.

Talent pools

In the rapidly changing environment in which Gasunie operates, managers have to satisfy demanding requirements. To ensure that they can meet those requirements, specific training programmes have been developed for them. We have training and educational programmes in various areas. These include traineeships, LEAD (Leadership, Empowerment and Development) courses for senior management, HighTech courses for managers in technical positions, and a campus recruiter who focuses on students in BBL9 apprenticeship training programmes at secondary vocational level.

Recruitment and selection procedures

Gasunie applies the following principles in recruitment, selection, advancement and promotion:

- In our company, everyone with the same competencies, agility and potential has an equal chance of being selected for a position.

- We do our best to ensure that no one feels discriminated against and we apply relevant and objective criteria when recruiting and selecting.

- We value differences.

- Our aim is to build a workforce that representatively reflects diversity in society.

- We offer people with poor job prospects additional opportunities.

People with poor job prospects

We want every talent to have the opportunity to develop. Gasunie offers internal budgets to have people with poor job prospects join departments on top of normal staffing levels for a maximum of two years, along with job coaching and support for both employees and their mentors. This allows us to take ample time to assess whether we can offer people with poor job prospects a workplace for the long term, in collaboration with Randstad RiseSmart.

Executive Board, Supervisory Board and management gender balance

In Gasunie’s view, an Executive Board and Supervisory Board should have a diverse and balanced composition. Having a balanced and diverse Executive Board and Supervisory Board contributes to the quality of the decision-making process and is also important from an equity perspective. A diverse board can have a positive impact on equity. Through job profiles and recruitment agency search queries, we explicitly request and focus on candidates who provide diversity.

Promotion of further education and training

At Gasunie, we offer everyone scope and equal opportunities to pursue personal and professional development. Through our offer of further education and training courses and our focus on personal development, we strive diligently to create equal opportunities for all. We collectively use a Sustainable Employability budget for programmes and investments that contribute to making and keeping employees healthy, such as ‘Master your Energy’. Gasunie wants fit, agile employees who can continue to adapt in a world that is constantly changing, and for this lifelong learning is essential. By employees honing their skill set and learning new skills, they increase their eligibility for career advancement and can take advantage of more opportunities.

Connected (LT)

Training

To engage all Gasunie employees in Gasunie’s DEI statement and policy, and to create awareness and commitment, employees need to have their attention focused on DEI on an ongoing basis. A few examples of how this is accomplished are:

- eLearning courses on DEI within Gasunie

- unconscious bias courses, general DEI training and guidance on dealing with diversity

- DEI during recruitment.

Workplace

Gasunie carefully weighs as many interests as possible in developing premises. For example, Gasunie sees to it that there are multiple restrooms for colleagues with reduced mobility. Premises are designed based on a vision that ensures an accessible workplace, quiet rooms, lactation rooms and low-stimulation spaces. Working from home is another option that can be used for employees with a neurodiverse condition, based on the principle that low-stimulation working environments are conducive to health and work.

Reference table

The table below shows our progress with regard to implementing the provisions of the European Sustainability Reporting Standards as published by the European Commission on 31 July 2023.

| 2025 | |||

|---|---|---|---|

| Description | Reference | Explanation | |

| ESRS 2 General disclosures | |||

| BP-1 | General basis for preparation of sustainability statements | General : Basis for preparation General: Consolidation |

The option in BP-1 5d and the exemption in BP-1 5e have not been used |

| BP-2 | Disclosures in relation to specific circumstances | General - Judgements, estimates and uncertainties General: Time horizons General: Results of the materiality assessment General: Connectivity table Circularity: Achievement of our goals Safety: Achievement of our goals Additional information: Sustainability Statement Appendix - Energy transition - Taxonomy- Table opex |

|

| GOV-1 | The role of the administrative, management and supervisory bodies | Governance: Corporate governance at Gasunie (Supervisory Board) Governance: Composition of the Executive Board Governance: Composition of the Supervisory Board Governance: Sustainability expertise of the Executive Board and Supervisory Board General: Policy and measurable targets Diversity: Achievements of our goals |

|

| GOV-2 | Information provided to and sustainability matters addressed by the undertaking’s administrative, management and supervisory bodies | Governance: Sustainability expertise of the Executive Board and Supervisory Board General: Policy and measurable targets General: Connectivity table |

|

| GOV-3 | Integration of sustainability-related performance in incentive schemes | Remuneration Report: Remuneration policy for the Executive Board (intro) Remuneration Report: Remuneration policy for the Executive Board - Variable remuneration |

|

| GOV-4 | Statement on due diligence | Additional information: Sustainability Statement Appendix - Due-diligence statement | |

| GOV-5 | Risk management and internal controls over sustainability reporting | Governance: Governance and risk management - Risk identification General: Policy and measurable targets General: Connectivity table |

|

| SBM-1 | Strategy, business model and value chain | We are Gasunie: Strategy 2030, heading towards realisation Vision 2040 (intro) We are Gasunie: Value chains Key figures: Key non-financial figures - achievement of our goals and forecasts Diversity: Key workforce figures |

|

| SBM-2 | Interests and views of stakeholders | General: Stakeholder interests and views | |

| SBM-3 | Material impacts, risks and opportunities and their interaction with strategy and business model | General: Connectivity table General: Results of the materiality assessment Energy transition: Financial impact |

Phasing option applied with respect to data item 48e in line with ESRS 1 Appendix C: List of phased-in Disclosure Requirements |

| IRO-1 | Description of the processes to identify and assess material impacts, risks and opportunities | General: Material themes Additional information Sustainability Statement Appendix - General - Structure of materiality assessment |

|

| IRO-2 | Disclosure requirements in ESRS covered by the undertaking’s sustainability statement | Additional information Sustainability Statement Appendix - General - Structure of materiality assessment Additional information Sustainability Statement Appendix - General - List of data points resulting from other EU legislation |

|

| MDR-P | Policies adopted to manage material sustainability matters | General: Policy and measurable targets Energy transition: Policy Emissions: Policy Circularity: Policy Security of supply: Policy Safety: Policy Diversity: Policy |

|

| MDR-A | Actions and resources in relation to material sustainability matters | Energy transition: Action plans Energy transition: Resources Emissions: Action plans Emissions: Resources Circularity: Action plans Circularity: Resources Security of supply: Action plans Security of supply: Resources Safety: Action plans Safety: Resources Diversity: Action plans Diversity: Resources Additional information Sustainability Statement Appendix - Diversity |

|

| MDR-M | Metrics in relation to material sustainability matters | Energy transition: Development of our forecasts Emissions:Achievement of our goals Circularity:Achievement of our goals Security of supply:Achievement of our goals Safety:Achievement of our goals Diversity:Achievement of our goals |

|

| MDR-T | Tracking effectiveness of policies and actions through targets | Energy transition: Our forecasts Emissions: Measurable targets Circularity: Measurable targets Security of supply: Measurable targets Safety: Measurable targets Diversity: Measurable targets |

|

| ESRS E1 Climate change | |||

| ESRS 2 GOV-3 | Integration of sustainability-related performance in incentive schemes | Remuneration report: Remuneration policy of the Executive Board - Reasoning behind variable remuneration | |

| S: E1-1 | Transition plan for climate change mitigation | We are Gasunie: Investment agenda Emissions: Policy Emissions: Action plans Emissions: Resources Emissions:Achievement of our goals |

|

| ESRS 2 SBM-3 | Material impacts, risks and opportunities and their interaction with strategy and business model | General: Connectivity table | |

| ESRS 2 IRO-1 | Description of the processes to identify and assess material climate-related impacts, risks and opportunities | General: Time horizons Emissions: Impacts, risks and opportunities Emissions: Policy - Climate transition plan |

|

| IRO: E1-2 | Policies related to climate change mitigation and adaptation | General: Policy and measurable targets Emissions: Policy |

|

| IRO: E1-3 | Actions and resources in relation to climate change policies | Emissions: Policy Emissions: Action plans Emissions: Resources Emissions:Achievement of our goals |

|

| M: E1-4 | Targets related to climate change mitigation and adaptation | Sustainability statement: Emissions - Policy Sustainability statement: Emissions - Action plans Sustainability statement: Emissions - Measurable targets Sustainability statement: Emissions -Achievement of our goals Additional information Sustainability Statement Appendix - Emissions |

|

| M: E1-5 | Energy consumption and mix | Emissions:Achievement of our goals Additional information Sustainability Statement Appendix - Emissions - Energy consumption and mix |

|

| M: E1-5 | Energy consumption and mix - Energy intensity based on net revenue | GTS, GUD and some of our holdings are regulated, meaning that public regulators determine what these companies are allowed to earn annually. We have therefore not included an energy intensity based on net earnings in our Sustainability Statement. | |

| M: E1-6 | Gross Scopes 1, 2, 3 and Total GHG emissions | Emissions: Measurable targets Emissions:Achievement of our goals Additional information Sustainability Statement Appendix - Emissions |

|

| M: E1-6 | GHG Intensity based on net revenu | GTS, GUD and some of our holdings are regulated, meaning that public regulators determine what these companies are allowed to earn annually. We have therefore not included an energy intensity based on net earnings in our Sustainability Statement. | |

| M: E1-7 | GHG removals and GHG mitigation projects financed through carbon credits | No material sub-sub-theme | |

| M: E1-8 | Internal carbon pricing | No material sub-sub-theme | |

| M: E1-9 | Anticipated financial effects from material physical and transition risks and potential climate-related opportunities | Phasing option applied with respect to Reporting Requirements 64-70 and Application Requirements 67-81 in line with ESRS 1 Appendix C: List of Phased-in Disclosure Requirements | |

| ESRS E4 Biodiversity | |||

| S: E4-1 | Transition plan and consideration of biodiversity and ecosystems in strategy and business model | For ESRS E4, we use the Quick-fix phasing-in provisions. See Additional information: Appendix sustainability declaration - Biodiversity\ | |

| ESRS 2 SBM-3 | Material impacts, risks and opportunities and their interaction with strategy and business model | ||

| ESRS 2 IRO-1 | Description of the processes to identify and assess biodiversity and ecosystems related impacts, risks and opportunities | ||

| IRO: E4-2 | Policies related to biodiversity and ecosystems | ||

| IRO: E4-3 | Actions and resources related to biodiversity and ecosystems | ||

| M: E4-4 | Targets related to biodiversity and ecosystems | ||

| M: E4-5 | Impact metrics related to biodiversity and ecosystems change | ||

| M: E4-6 | Anticipated financial effects from biodiversity and ecosystem-related risks and opportunities | ||

| ESRS E5 Resource use and circular economy | |||

| ESRS 2 IRO-1 | Description of the processes to identify and assess material resource use and circular economy-related impacts, risks and opportunities | Circularity: Impacts, risks and opportunities | |

| IRO: E5-1 | Policies related to resource use and circular economy | General: Policy and measurable targets Circularity: Policy Circularity: Measurable targets |

|

| IRO: E5-2 | Actions and resources related to resource use and circular economy | Circularity: Policy Circularity: Action plans Circularity: Measurable targets |

|

| M: E5-3 | Targets related to resource use and circular economy | Circularity: Policy Circularity: Measurable targets |

|

| M: E5-4 | Resource inflows | Circularity:Achievement of our goals Additional information: Sustainability Statement Appendix - Circularity |

|

| M: E5-5 | Resource outflows | No material sub-sub-theme | |

| M: E5-6 | Anticipated financial effects from resource use and circular economy-related impacts, risks and opportunities |

Phasing option applied with respect to Reporting Requirements 41-43 and Application Requirements 34-36 in line with ESRS 1 Appendix C: List of Phased-in Disclosure Requirements | |

| ESRS S1 Own workforce | |||

| ESRS 2 SBM-2 | Interests and views of stakeholders | General: Stakeholder interests and views | |

| ESRS 2 SBM-3 | Material impacts, risks and opportunities and their interaction with strategy and business model | Governance: Corporate governance at Gasunie (Works Council ) Governance: Corporate governance at Gasunie - Codes and schemes (Conduct Guidelines – Working Together) General: Connectivity table Safety: Policy Diversity: Policy Additional information Sustainability Statement Appendix - General - Structure of materiality assessment |

|

| IRO: S1-1 | Policies related to own workforce | Governance: Corporate governance at Gasunie - Codes and schemes (Speak Up-scheme, Confidential counsellors and Conduct Guidelines - Working Together) Safety: Policy Diversity: Policy Diversity: Action plans |

|

| IRO: S1-2 | Processes for engaging with own workers and workers’ representatives about impact | Governance: Corporate governance at Gasunie (Works Council ) Governance: Corporate governance at Gasunie - Codes and schemes (Conduct Guidelines – Working Together) Safety: Policy Diversity: Action plans Diversity: Policy Additional information: Report of the Works Council - Talks with the employees across the country |

|

| IRO: S1-3 | Processes to remediate negative impacts and channels for own workers to raise concerns | Governance: Corporate governance at Gasunie - Codes and schemes | |

| IRO: S1-4 | Taking action on material impacts on own workforce, and approaches to mitigating material risks and pursuing material opportunities related to own workforce, and effectiveness of those actions | Safety: Action plans Diversity: Action plans Safety: Measurable targets Diversity: Measurable targets Safety: Resources Diversity: Resources Safety:Achievement of our goals Diversity: Measurable targets Additional information: Report of the Works Council - Talks with the employees across the country |

|

| M: S1-5 | Targets related to managing material negative impacts, advancing positive impacts, and managing material risks and opportunities |

General: Policy and measurable targets Safety: Measurable targets Diversity: Measurable targets Safety:Achievement of our goals Diversity:Achievement of our goals |

|

| M: S1-6 | Characteristics of the undertaking’s employees | Diversity: Key workforce figures | |

| M: S1-7 | Characteristics of non-employee workers in the undertaking’s own workforce |

Diversity: Key workforce figures | |

| M: S1-8 | Collective bargaining coverage and social dialogue | No material sub-sub-theme | |

| M: S1-9 | Diversity metrics | Diversity: Measurable targets Diversity:Achievement of our goals |

|

| M: S1-10 | Adequate wage | No material sub-sub-theme | |

| M: S1-11 | Social protection | No material sub-sub-theme | |

| M: S1-12 | Persons with disabilities | No material sub-sub-theme | |

| M: S1-13 | Training and skills development metrics | No material sub-sub-theme | |

| M: S1-14 | Health and safety metrics | Safety: Policy Safety: Measurable targets Safety: Achievement of our goals |

Phasing option applied with respect to reporting requirements 88 d, 88 e and 89 and application requirements 94 in line with ESRS 1 Appendix C: List of phased-in Disclosure Requirements |

| M: S1-15 | Work-life balance metrics | No material sub-sub-theme | |

| M: S1-16 | Compensation metrics (pay gap and total compensation) | No material sub-sub-theme | |

| M: S1-17 | Incidents, complaints and severe human rights impacts | No material sub-sub-theme | |

| ESRS S2 Workers in the value chain | |||

| ESRS 2 SBM 2 | Interests and views of stakeholders | For ESRS S2, we use the Quick-fix phasing-in provisions. See Safety. | |

| ESRS 2 SBM 3 | Material impacts, risks and opportunities and their interaction with strategy and business model | ||

| IRO: S2-1 | Policies related to value chain workers | ||

| IRO: S2-2 | Processes for engaging with value chain workers about impacts | ||

| IRO: S2-3 | Processes to remediate negative impacts and channels for value chain workers to raise concerns | ||

| IRO: S2-4 | Taking Action on material impacts, and approaches to mitigating material risks and pursuing material opportunities related to value chain workers, and effectiveness of those actions and approaches | ||

| M: S2-5 | Targets related to managing material negative impacts, advancing positive impacts, and managing material risks and opportunities | ||

Due diligence statement

| Core elements of due diligence | Paragraphs in the sustainability statement |

|---|---|

| a) Embedding due diligence in governance, strategy and business model | General: Policy and measurable targets General: Material topics - Results of materiality assesment Remuneration report: Remuneration policy for the Executive Board - Variable remuneration |

| b) Engaging with affected stakeholders in all key steps of the due diligence | General: Policy and measurable targets General: Results of materiality assesment |

| c) Identifying and assessing adverse impacts | Additional information: Sustainability Statement Appendix - Structure of the materiality assessment - step 3: from mediumlist to shortlist General: Connectivity table |

| d) Taking actions to address those adverse impacts | Emissions: Action plans Circularity: Action plans Security of supply: Action plans Safety: Action plans Diversity: Action plans Additional information: Sustainability Statement Appendix - Biodiversity - Action plans |

| e) Tracking the effectiveness of these efforts and communicating | Emissions: Achievement of our goals Circularity: Achievement of our goals Security of supply: Achievement of our goals Safety: Achievement of our goals Diversity: Achievement of our goals |

List of data points resulting from other EU legislation

| Disclosure Requirement and related datapoint | SFDR reference | Pillar 3 reference | Benchmark regulation reference | EU Climate Law reference | Material / Not material | Paragraphs in the sustainability statement |

|---|---|---|---|---|---|---|

| ESRS 2 GOV-1 Board's gender diversity paragraph 21 (d) | Indicator n.13 of Table 1 of Annex 1 | Not applicable | Commission Delegated Regulation (CDR) (EU) 2020/1816, Annex II | Not applicable | Material | Diversity: Achievements of our goals |

| ESRS 2 GOV-1 Percentage of board members who are independent paragraph 21 e | Not applicable | Not applicable | CDR (EU) 2020/1816, Annex II | Not applicable | Material | Governance: Corporate governance at Gasunie (Supervisory Board) |

| ESRS 2 GOV-4 Statement on due diligence paragraph 30 | Indicator no. 10 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Material | Additional information: Appendix Sustainability report - Due diligence statement |

| ESRS 2 SBM-1 Involvement in activities related to fossil fuel activities paragraph 40 (d) i | Indicator no. 4 of Table 1 of annex I | Article 449a Capital Requirements Regulation – CRR; Template 1: Banking book-Climate Change transition risk: Credit quality of exposures by sector, emissions and residual maturity | CDR (EU) 2020/1816, Annex II | Not applicable | Material | Key figures |

| ESRS E1-1 Transition plan to reach climate neutrality by 2050 paragraph 14 | Not applicable | Not applicable | Not applicable | Regulation (EU) 2021/1119, art. 2, paragraph 1 | Material | Emissions: Policy - Climate Transition Plan |

| ESRS E1-1 Undertakings excluded from Paris-aligned Benchmarks paragraph 16 (g) | Not applicable | Article 449a Capital Requirements Regulation – CRR; Template 1: Banking book-Climate Change transition risk: Credit quality of exposures by sector, emissions and residual maturity | CDR (EU) 2020/1818, art. 12, paragraph 1, points d) t/m g), and art. 12, paragraph 2 | Not applicable | Not applicable | |

| ESRS E1-4 GHG-emission reduction targets paragraph 34 | Indicator no. 4 of Table 2 of annex I | Article 449a Capital Requirements Regulation – CRR; Template 3 Climate change transition risk - alignment metrics for the banking book | CDR (EU) 2020/1818, art. 6 | Not applicable | Material | Emissions:Measurable targets Additional information: Appendix Sustainability report - Emissions |

| ESRS E1-5 Energy consumption from fossil sources disaggregated by sources (only high climate impact sectors) paragraph 38 | Indicator no. 5 of Table 1 and indicator no. 5 of Table 2 of annex I | Not applicable | Not applicable | Not applicable | Material | Additional information: Appendix Sustainability report - Emissions - Energy consumption and mix |

| ESRS E1-5 Energy consumption and mix paragraph 37 | Indicator no. 5 of Table 1 of annex I | Not applicable | Not applicable | Not applicable | Material | Additional information: Appendix Sustainability report - Emissions - Energy consumption and mix |

| ESRS E1-5 Energy intensity associated with activities in high climate impact sectors paragraphs 40 to 43 | Indicator no. 6 of Table 1 of annex I | Not applicable | Not applicable | Not applicable | Not material | GTS, GUD and some of our holdings are regulated, meaning that public regulators determine what these companies are allowed to earn annually. We have therefore not included an energy intensity based on net earnings in our Sustainability Statement. |

| ESRS E1-6 Gross Scope 1, 2, 3 and Total GHG emissions paragraph 44 | Indicators nrs. 1 and 2 of Table 1 of annex I | Article 449a Capital Requirements Regulation – CRR; Template 3 Climate change transition risk - alignment metrics for the banking book | CDR (EU) 2020/1818, art. 5, paragraph 1, art. 6 and art. 8, paragraph 1 | Not applicable | Material | Emissions: Achievement of our goals - ESRS tables for scope 1, 2 and 3 |

| ESRS E1-6 Gross GHG emissions intensity paragraphs 53 to 55 | Indicator no. 3 of Table 1 of annex I | Article 449a Capital Requirements Regulation – CRR; Template 3 Climate change transition risk - alignment metrics for the banking book | CDR (EU) 2020/1818, art. 8, paragraph 1 | Not applicable | Not material | GTS, GUD and some of our holdings are regulated, meaning that public regulators determine what these companies are allowed to earn annually. We have therefore not included an energy intensity based on net earnings in our Sustainability Statement. |

| ESRS E1-9 Exposure of the benchmark portfolio to climate-related physical risks paragraph 66 | Not applicable | Not applicable | CDR (EU) 2020/1818, annex II; CDR (EU) 2020/1816, annex II | Not applicable | Not material | Phasing option applied with respect to Reporting Requirements 64-70 and Application Requirements 67-81 in line with ESRS 1 Appendix C: List of Phased-in Disclosure Requirements |

| ESRS E1-9 Disaggregation of monetary amounts by acute and chronic physical risk paragraph 66 (a) ESRS E1-9 Location of significant assets at material physical risk paragraph 66 (c). |

Not applicable | Article 449a CRR; Final ITS, paragraphs 46 and 47; Template 5: Banking book - Climate change physical risk: Exposures subject to physical risk. | Not applicable | Not applicable | Not material | Phasing option applied with respect to Reporting Requirements 64-70 and Application Requirements 67-81 in line with ESRS 1 Appendix C: List of Phased-in Disclosure Requirements |

| ESRS E1-9 Breakdown of the carrying value of its real estate assets by energy-efficiency classes paragraph 67 (c). | Not applicable | Article 449a CRR; Final ITS, paragraph 34; Template 2: Banking book -Climate change transition risk: Loans collateralised by immovable property -Energy efficiency of the collateral | Not applicable | Not applicable | Not material | Phasing option applied with respect to Reporting Requirements 64-70 and Application Requirements 67-81 in line with ESRS 1 Appendix C: List of Phased-in Disclosure Requirements |

| ESRS E1-9 Degree of exposure of the portfolio to climate-related opportunities paragraph 69 | Not applicable | Not applicable | CDR (EU) 2020/1818, annex II | Not applicable | Not material | Phasing option applied with respect to Reporting Requirements 64-70 and Application Requirements 67-81 in line with ESRS 1 Appendix C: List of Phased-in Disclosure Requirements |

| ESRS S1-1 Human rights policy commitments paragraph 20 | Indicator no. 9 of Table 3 and indicator no. 11 of Table 1 of annex I | Not applicable | Not applicable | Not applicable | Material | Governance: Corporate governance at Gasunie - Codes and schemes |

| ESRS S1-1 Due diligence policies on issues addressed by the fundamental International Labor Organisation Conventions 1 to 8, paragraph 21 | Not applicable | Not applicable | Not applicable | Not applicable | Material | Governance: Corporate governance at Gasunie - Codes and schemes |

| ESRS S1-1 processes and measures for preventing trafficking in human beings paragraph 22 | Indicator no. 11 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Not material | |

| ESRS S1-1 workplace accident prevention policy or management system paragraph 23 | Indicator no. 1 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Material | Safety: Policy |

| ESRS S1-14 Number of fatalities and number and rate of work-related accidents paragraph 88 (b) and (c) | Indicator no. 2 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Material | Safety: Achievement of our goals |

| ESRS S1-14 Number of days lost to injuries, accidents, fatalities or illness paragraph 88(e) | Indicator no. 3 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Material | Phasing option applied with respect to reporting requirements 88 d, 88 e and 89 and application requirements 94 in line with ESRS 1 Appendix C: List of phased-in Disclosure Requirements |

| ESRS 2- SBM3 – S2 Significant risk of child labour or forced labour in the value chain paragraph 11 (b) | Indicator nrs. 12 and 13 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Phasing option applied | |

| ESRS S2-1 Human rights policy commitments paragraph 17 | Indicator no. 9 of Table 3 and indicator no. 11 of Table 1 of annex I | Not applicable | Not applicable | Not applicable | Phasing option applied | |

| ESRS S2-1 Policies related to value chain workers paragraph 18 | Indicator nrs. 11 and 4 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Phasing option applied | |

| ESRS S2-1 Non-respect of UNGPs on Business and Human Rights principles and OECD guidelines paragraph 19 | Indicator no. 10 of Table 1 of annex I | Not applicable | CDR (EU) 2020/1816, annex II; CDR (EU) 2020/1818, art. 12, paragraph 1 | Not applicable | Phasing option applied | |

| ESRS S2-1 Due diligence policies on issues addressed by the fundamental International Labor Organisation Conventions 1 to 8, paragraph 19 | Not applicable | Not applicable | CDR (EU) 2020/1816, annex II | Not applicable | Phasing option applied | |

| ESRS S2-4 Human rights issues and incidents connected to its upstream and downstream value chain paragraph 36 | Indicator no. 14 of Table 3 of annex I | Not applicable | Not applicable | Not applicable | Phasing option applied |

Report of the Works Council

Foreword by the chair of the Works Council

For the Works Council, the year 2025 was a year of both adapting to and overseeing an organisation in transition. In addition to our regular activities, which include responding to requests for advice and consent, the year revolved primarily around the implementation of the new operating model, which constituted a large-scale and impactful organisational change the likes of which we had not experienced at Gasunie in at least ten years.

Implementation of the new operating model

As soon as the very first outlines of the design of the new operating model emerged, the Works Council engaged in intensive and frequent consultations with the Executive Board and with the Transformation Team that prepared the implementation of the new operating model. This early, constructive involvement allowed us to raise points for attention during the design phase and exert real influence on the new organisational structure, both in terms of its setup and the conditions for collaboration, governance and decision-making. This aligns with the approach established in our responses to requests for advice on the operating model, which was to ensure clear roles and responsibilities, consistent processes and a management philosophy that promotes decisive action, with a specific focus on culture and conduct.

There is more to a change of this scale than just drawing lines on an organisational chart. Since behavioural and cultural aspects are critical for success, the Works Council consistently stressed the importance of the interconnection between structure, leadership and collaboration. In addition, we advised the management to lead by example, to ensure that the new ways of working actually take hold in practice.

Culture and conduct: start of the culture programme

The first of October saw the launch of the culture programme associated with the implementation of the new operating model, in which the Works Council fulfils a sounding board role. We provide feedback, both solicited and unsolicited, and help interpret signals from the organisation at an early stage. Our approach has remained consistent throughout, as we called on the management to make clear choices, embed them in simple, workable agreements and ensure visible, consistent follow-up, especially where value chain collaboration and mandates intersect.

Regular employee participation

In addition to the transformation, we handled a series of regular requests for advice and consent in 2025. These processes saw the Works Council, as per usual, assess the necessity, proportionality, support and feasibility of changes proposed by the management. Where necessary, we formulated preconditions and mitigating measures.

Talks with employees across the country

To stay connected with all employees in the company, the Works Council organises various meetings at locations across the Netherlands. These meetings always take the form of an employee lunch, during which we can talk personally with employees and discuss various matters at length. This provides valuable insights we can use when handling requests for advice and requests for consent and which, when appropriate, we raise in consultations with the management of a particular department or with HR. Topics that come up repeatedly in these consultations include workload, change fatigue, the growth of the company and, of course, implementation of the new operating model. In addition, we always ask about the current state of affairs with respect to safety, accommodation and efficiency. After all, these continue to be our key focus areas. In 2025, we held 8 meetings with employees (2024: 7).

Executive Board changes

The year 2025 saw significant changes at the top of the organisation. In January, the Works Council welcomed interim CFO Jan Boekelman to the company. Over the course of the year, the Works Council issued a positive advisory opinion on the appointments of COO Marc van der Linden and CTO Bart Leenders. Finally, the Works Council also issued a positive advisory opinion on the appointment of CFO Katie Slipper, effective January 2026.

- he introductory meetings with Jan Boekelman were positive. The appointment of an interim CFO aligned seamlessly with the need for continuity in the financial domain.

- Regarding the appointment of COO Marc van der Linden, the Works Council issued a positive advisory opinion following consultations that focused on the management of capital-intensive projects, delivering predictable results, and attention to culture and leadership.

- The Works Council also issued positive advisory opinions on CTO Bart Leenders and CFO Katie Slipper. These appointments address the need to strengthen our technical and financial leadership for the next phase of the energy transition.

What the Works Council considered essential

- Early involvement in design choices and the implementation approach, ensuring feasibility and workability for employees;

- Interconnection of structure, culture and behaviour. Without clear leadership and leading by example, the operating model will not take hold. The Works Council has made a point of highlighting this throughout the year;

- Continuity in governance amidst board changes, balancing internal knowledge with external renewal.

Outlook for 2026

The coming period will be about making the new operating model and working method work in practice. This includes optimising processes, improving role clarity, actually using mandates and aiming for predictable results while allowing space to learn and adjust. The Works Council will continue to be a critical ally in this process. We will be constructive where possible, and tenacious when we have to be. We will continue to pursue the culture programme, monitor the effects of the reorganisation on workload and employee well-being, and maintain close dialogue with colleagues, the Executive Board and the Transformation Team.

A word of thanks

The Works Council would like to thank all colleagues for their openness and commitment, the Executive Board and the Transformation Team for their close collaboration, and fellow employee representatives for their professional support. The transition posed considerable challenges for all of us, and so we truly value the resilience and professionalism shown in 2025.

Risk management

| Title | Description |

|---|---|

| Inappropriate culture and behaviour | The risk of Gasunie having to deal with inappropriate culture and behaviour. A lack of insight into and control over appropriate behaviour leads to the risk of an inappropriate culture arising. This can lead to business ethics being undermined, financial and operational delays, and damage to our reputation. |

| Disruptions in the supply chain | The risk of Gasunie facing disruptions in the supply chain, dute to problems at suppliers or in logistics. Leading to delays in projects, higher operating expenses and/or customer dissatisfaction due to delayed deliverables. |

| Third-party risk | The risk of Gasunie being confronted with disruptions and adverse events caused by third parties. These are the result of insufficient screening and inadequate due diligence when outsourcing to and collaborating with third parties (suppliers, contractors, etc.) and poor performance on the part of third parties. This leads to disruptions in business operations, fines/sanctions, fraudulent activities and/or reputational damage. |

| Regulatory risk | The risk of Gasunie facing (unexpected) significant changes to requirements and obligations. This is caused by amendments to regulations by bodies such as ACM and BNetzA. It could result in lower revenue, increased costs, fines/sanctions and/or reputational damage. |

| Higher borrowing costs | The risk of Gasunie being confronted with significantly higher borrowing costs. This is caused by changing conditions on the financial markets and/or the implementation of the strategic investment agenda. This could lead to lower returns and/or a lower credit rating. |

| Non-compliance with laws and regulations | The risk of Gasunie not complying with laws and regulations. Caused by insufficient awareness, lack of compliance training and/or understaffing in supervisory functions. It could result in legal sanctions, fines, increased time pressure, reputational damage and/or business disruptions. |

| Technological risk | The risk of Gasunie facing reduced demand for transport, storage and terminal capacity. This is caused by technological breakthroughs (e.g. in battery technology) that fundamentally change the role of molecules and/or advances that increase decentralisation of supply and demand. It could result in early write-down of assets and/or lower revenue. |

| Interruption of gas transport | The risk of Gasunie being faced with an interruption of gas transport. This is due to drastic climate change and weather conditions, and/or unforeseen operational disruptions and events caused by social unrest. It could result in interruptions to operations, damage to operating assets, potential safety hazards for the surrounding area around operating assets, delays in project implementation and significant costs for repairs and risk management. |

Disclaimer

Where this report refers to ‘we’ or ‘us’, this means the activities of N.V. Nederlandse Gasunie, unless otherwise explicitly specified. Activities of the two segments of Gasunie always refer to Gasunie Deutschland (GUD) and Gasunie Transport Services (GTS).

In the event of inconsistencies or differences of interpretation between the Dutch report and the English report, the Dutch report shall prevail.